| Improve Your Business: Basics (ILO, 1999, 188 p.) | |||||

| COSTING | |||||

| (introduction...) | |||||

| Know your costs | |||||

| Costing for a manufacturer or service operator | |||||

| Costing for a retailer or wholesaler | |||||

| Review | |||||

| Summary | |||||

| What did you learn in this chapter? | |||||

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||

IN THIS CHAPTER YOU WILL LEARN

Determine what it costs to run your business

|

NOTE |

Since this book is intended for use in many different countries, we have used the term “NU” in the examples to represent an imaginary “National Unit of currency” |

WHAT ARE COSTS?

Every business has costs. Costs are all the money your business spends to make and sell your products or services. Here are some examples of costs:

· Salaries and wages to the employees are costs to the business.

· Electricity for the lights, machines and other equipment is a cost to the business.

· Raw materials bought to make into products are a cost to the business.

If you are a service operator, a retailer or a wholesaler, you may not have exactly the same costs as a manufacturer. But most businesses have costs for materials, labour, electricity, rent, transport, and so on.

WHAT IS COSTING?

Costing is the way you calculate the total costs of making and selling a product or providing a service. Many businesses do not know all their costs and therefore cannot do their costing properly.

|

THINK ABOUT THESE TWO BUSINESSES: · A pottery: Clayworks Pottery make tea cups. They do not know their costs but they do not worry too much about costs, they only want to be cheaper than their competitors so they sell more. Most other potteries charge 4.50 Nil for a tea cup so Clayworks decide to set their price at 3.90 NU. · A metalworks business: A customer asks for a quotation for 5 door frames. The material for one door frame costs 65.00 NU. The Metalworks Company decide to charge 70.00 NU for each frame. It is a low price but it is more than the cost of the materials so they think that they will still make a profit. 1. Is there a problem with the way Clayworks Pottery do the

costing of their tea cups? Please explain why or why

not? 2. Is there a problem with the way The Metalworks Company do

the costing of their door frames? Please explain why or why

not? |

|

1. Yes, there is a problem with the way Clayworks Pottery do the costing of tea cups. They set a price which is lower than the other potteries’ prices. They do not know if their total costs for a tea cup are higher than their price of 3.90 NU. Clayworks Pottery do not know if the tea cups give their business a profit or a loss. 2. Yes, there is a problem with the way The Metalworks Company do the costing of their door frames. They know the direct material costs for a door frame. But they think that the 5.00 NU they add to the cost of materials is profit. They forget about other costs that their business has, for example: · labour costs for their employees making the door frames The Metalworks Company do not know if the price of 70.00 NU gives the business a profit or a loss. |

HOW CAN COSTING IMPROVE YOUR BUSINESS?

Costing helps you to set prices

When you know your total costs, you can set prices which will give your business a profit.

Costing helps you to reduce and control your costs

When you know all your costs, you can work out better and cheaper ways to make and sell your products or services.

Costing helps you to make better decisions about your business

When you know the total costs for each type of product or service, you can make better decisions about which products or services to sell so that your business makes the highest profit.

Costing helps you to plan for the future

When you know all your costs, you can make plans for your business. For example, you need to know all your costs before you can make a Sales and Costs Plan or a Cash Flow Plan.

DIFFERENT TYPES OF COSTS

Before you can do costing, it is necessary to understand the different types of costs a business has. All businesses have two types of costs:

· direct costs, and

· indirect costs.

|

Direct |

+ |

Indirect |

= |

TOTAL COSTS |

You must understand the different types of costs to be able to calculate the total costs and do the costing for each product or service your business makes or sells.

Direct costs

For a manufacturer or service operator, direct costs are all costs that can be directly related to:

· the products or services you make or sell, or

· the production of those products or services.

For a retailer or wholesaler, direct costs are the costs for buying goods to resell.

To be counted as direct costs, the costs must also be:

· easy to calculate

· big enough to add a considerable amount to the total direct costs.

For example, Reliable Tailors make protective coats. Fabric and buttons are direct costs for making a protective coat because:

· they become part of the coat

· the amounts of fabric and buttons for each coat are easy to calculate

· the costs of fabric and buttons are big enough to add a considerable amount to the total direct costs of a coat.

Reliable Tailors have employees working full time sewing protective coats. Those employees’ wages are direct costs because:

· their work is directly related to the production of coats

· the time they spend making coats is easy to calculate

· their wages are big enough to add a considerable amount to the total direct costs of a coat.

Reliable Tailors have to pay for two things that are directly related to the production of protective coats:

· materials

· labour.

So you can see there are two different types of direct costs:

· direct material costs

· direct labour costs.

Figure

Direct material costs

Direct material costs are what your business spends on materials that become part of, or are directly related to, the products or services you make or sell.

To be counted as a direct material cost:

· the amount of material must be easy to calculate

· the cost of the material must be big enough to add a considerable amount to the total direct material costs.

Here are examples of direct material costs for different businesses:

· At The Metalworks Company, the sheets of metal, hinges and bolts become part of the door frames. The amount of each material for one door frame is easy to calculate. The cost of each material is big enough to add a considerable amount to the total direct material costs of the business. So the costs of sheet metal, hinges and bolts are direct material costs for the business.· Reader’s Bookshop does not make products. They buy stationery, books and other goods to resell. For a retailer or wholesaler, the costs of buying goods to resell are direct material costs.

Direct labour costs

Direct labour costs are all the money your business spends on wages, salaries and benefits for the employees who work in the production of your products or services. Retailers and wholesalers, who do not make products or provide services, do not have direct labour costs.

To be counted as a direct labour cost:

· the time spent on making the product must be easy to calculate

· the cost of the direct labour must be big enough to add a considerable amount to the total direct labour costs.

Here are examples of direct labour costs for different businesses:

· At The Metalworks Company, the employees’ work is production of metal products. The time spent making each product is easy to calculate. The wages paid for the work are big enough to add a considerable amount to the total direct labour costs. So the wages the business pays to the employees are direct labour costs for the business.· Reader’s Bookshop does not have any employees working directly in making products. So they do not have any direct labour costs.

Indirect costs

Businesses do not only have direct costs. All businesses also have costs for running the business, for example rent, electricity, transport, licences, repairs and maintenance. These types of costs are called indirect costs.

Indirect costs are all other costs, except direct costs, that you have for running your business. Indirect costs are normally not directly related to one particular product or service. They are costs for the whole business.

Here are some examples of indirect costs:

|

|

|

|

Costs for buildings and equipment, for example rent, electricity and water, maintenance, repairs, service and insurance are indirect costs. |

Costs for transport for buying materials or goods, visiting suppliers or customers, and for delivering goods to customers are indirect costs. |

Costs for wages of employees or owners who do not work directly in the production of goods or services are indirect costs. For example, wages of sales staff, messengers, cleaners and security guards are indirect costs. For retailers and wholesalers, all salaries and wages are indirect costs. These costs are called indirect labour costs.

Some costs that would normally be calculated as direct costs can become indirect costs. Here is an example:

To make coats, Reliable Tailors use thread. But they have decided that thread is an indirect cost and not a direct cost because:

· the amount of thread they use to make one protective coat is very small and difficult to calculate· the cost of the small amount of thread they use to make one coat is not big enough to add a considerable amount to the total direct material costs.

You can see that there are different types of costs that make up the total costs of a product or service.

|

Direct |

+ |

Direct |

+ |

Indirect |

= |

TOTAL COSTS |

|

If you are a retailer or wholesaler, go to Costing for a retailer or wholesaler. |

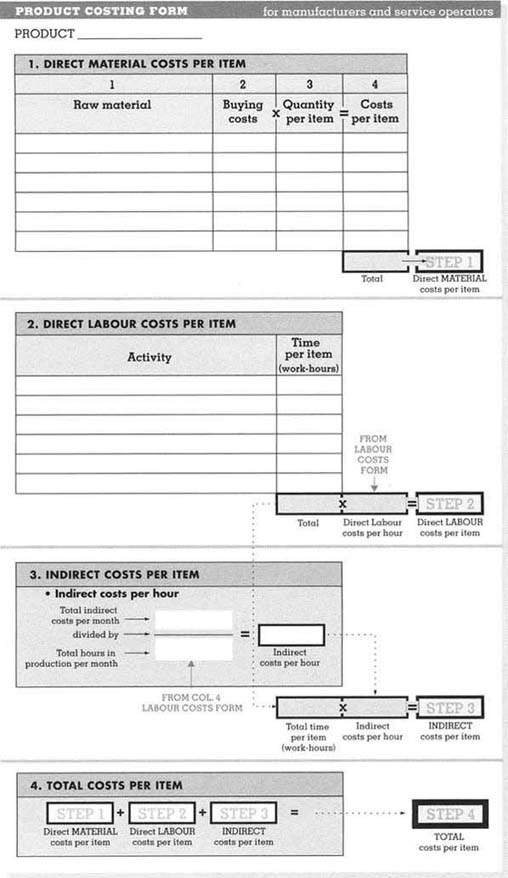

To explain how a manufacturer or service operator does costing we use Reliable Tailors as an example. Reliable Tailors make different types of garments such as protective coats and overalls. To help them calculate all the costs for one product they use a Product Costing Form. The Product Costing Form follows 4 steps:

|

Step 1 | |

Step 2 | |

Step 3 | |

Step 4 |

|

Direct |

+ |

Direct |

+ |

Indirect |

= |

TOTAL COSTS |

The next page shows a Product Costing Form. Reliable Tailors also use a Labour Costs Form to help them with their calculations.

They use the Labour Costs Form in Step 2.

|

COSTING FOR | |

|

| |

|

STEP 1. |

Calculate direct |

| | |

|

STEP 2. |

Calculate direct |

| | |

|

STEP 3. |

Calculate |

| | |

|

STEP 4. |

Add up |

|

|

Reliable Tailors is a manufacturer. If you are a service operator, use the Product Costing Form and the same 4 steps for the costing of each of your services. You can do an exercise for a service operator. |

Figure

STEP 1. CALCULATE DIRECT MATERIAL COSTS

|

COSTING FOR | |

|

| |

|

STEP 1. |

Calculate direct |

| | |

|

STEP 2. |

Calculate direct |

| | |

|

STEP 3. |

Calculate |

| | |

|

STEP 4. |

Add up |

Calculate the costs of all materials:

· that become part of, or are directly related to, the product or service

· that are easy to calculate and have a big enough cost to be counted.

You can see how Reliable Tailors use the Product Costing Form to calculate the direct material costs for one protective coat to be 30.40 NU.

Here are some notes to help you complete Step 1 of the Product Costing Form to work out the direct material costs per item:

Column 1. Raw material

In column 1 on the Product Costing Form, write down the different raw materials that become part of the product or service. Only include materials that are easy to calculate and have a big enough cost to be counted.

Reliable Tailors write down fabric and buttons. They also use thread but:

· it is difficult to calculate how much thread they need for one coat

· the thread needed for one coat costs very little.

So Reliable Tailors have decided that thread is not a direct material cost for making protective coats. At Reliable Tailors, thread for making coats is counted as an indirect cost. You can see how Reliable Tailors include thread in their indirect costs.

Column 2. Buying costs

In column 2 on the Product Costing Form, write down the cost of buying one unit of each raw material.

Column 3. Quantity per item

In column 3 on the Product Costing Form, write down how much you need of each raw material to make one item. Remember to include wastage.

Most businesses have some wastage. For example:

· Reliable Tailors have small pieces of fabric left over.

· A carpenter has off-cuts of wood wasted.

· A tinsmith gets bits of metal that are too small to use.

Wastage is a cost to your business because you have paid for the raw materials that are wasted. Work out how much waste you normally have for one item. Add this amount to the quantity of material you need to make the item.

Column 4. Costs per item

In column 4 on the Product Costing Form, write down the cost of each material needed to make one item. To calculate this cost, multiply the buying costs (column 2) by the quantity needed for one item (column 3).

Total

When you have worked out the cost of each raw material needed to make one item, add up the amounts in column 4. This total gives you the total direct material costs for the item.

STEP 2. CALCULATE DIRECT LABOUR COSTS

|

COSTING FOR | |

|

| |

|

STEP 1. |

Calculate direct |

| | |

|

STEP 2. |

Calculate direct |

| | |

|

STEP 3. |

Calculate |

| | |

|

STEP 4. |

Add up |

Work out the costs of wages, salaries and benefits for the employees who work directly in the production of the product or service.

Every business needs information on all their labour costs. To help you calculate labour costs for your business, you can use a Labour Costs Form.

On the Labour Costs Form, you write information about each person working in your business, for example, working hours per month, wage per month and time in production per month.

You need this information to:

· calculate the direct labour costs per hour (on the Labour Costs Form)

· calculate the direct labour costs per item (on the Product Costing Form).

|

|

You only need one Labour Costs Form for the whole business. You use the information in that form to calculate the cost of all your products or services. |

Reliable Tailors have nine employees. Most of them work in production, but some of them are not directly involved in the production. That is important to know when you calculate the direct labour costs.

First, Reliable Tailors fill in the Labour Costs Form. Then they use the information to work out the direct labour costs for one protective coat on the Product Costing Form.

Here is the Labour Costs Form for Reliable Tailors:

Figure

Column 1. Employee

In column 1 on the Labour Costs Form, write down the name of each person working in the business. You can also write down the type of work they do.

If you are the owner, you must remember to include yourself. For example, at Reliable Tailors, Mr Anderson and Mrs Hall are the owners:

· Mr Anderson does supervision and sewing.

· Mrs Hall does sales and administration.

Column 2. Total working hours per month

In column 2 on the Labour Costs Form, write down the number of hours each person works in the business per month.

At Reliable Tailors, most employees work 160 hours per month.

But two employees do not work 160 hours per month:

· Miss Peters assists with record-keeping. She only works 40 hours per month.

· Mr Hunter is very skilled at sewing. He works extra hours when there is a lot of work. With overtime, Mr Hunter usually works 180 hours per month.

Column 3. Total monthly pay

In column 3 on the Labour Costs Form, write down how much each person gets paid per month.

Owner’s salary is also part of the labour costs for a business. It is important that the owner writes down how much the business pays him or her per month. For example, Mr Anderson and Mrs Hall pay themselves 1000 NU each per month.

The Labour Costs Form is divided into two parts:

· Direct labour costs (columns 4 and 5)

· Indirect labour costs (columns 6 and 7)

Direct labour costs

Columns 4 and 5 on the Labour Costs Form give you information about the costs for employees who work directly in the production of your products or services. Their wages, salaries and benefits are direct labour costs.

Column 4. Hours in production per month

In column 4 on the Labour Costs Form, write down how many hours each person works in production per month.

At Reliable Tailors, Mr Wilson, Mr Hunter, Mrs Jones, Mrs Preston and Miss Turner spend all their time working in production. So, for each of them, the number of hours in column 4 is the same as the total working hours per month in column 2.

Mrs Hall, Mr Smith and Miss Peters do not work in production. They do other kinds of work. Their salaries and wages are indirect labour costs (see column 6).

Some people work in production and also do other jobs that are not directly related to the production of a particular product or service. For example, look at the information on the Labour Costs Form for Mr Anderson:

· Half of his time, 80 hours per month, Mr Anderson does sewing. He works directly in production. His salary for this work is a direct labour cost.· The other half of his time, 80 hours per month, Mr Anderson supervises the production of all the garments that Reliable Tailors make. His salary for this work is an indirect labour cost (see column 6).

Column 5. Pay for time in production

In column 5 on the Labour Costs Form, write down how much of each person’s monthly pay is for time spent working in production. If a person works full-time in production, the whole wage is a direct labour cost. If a person works part-time in production, divide the wage into direct labour costs and indirect costs.

For example at Reliable Tailors:

· Mr Anderson’s total salary is 1000 NU.

· He spends half his time in production and half his time supervising.

· Half his salary, 500 NU, is for time spent in production and is a direct labour cost. So 500 NU is written down as pay for time in production in column 5 on the Labour Costs Form.

Indirect labour costs

Columns 6 and 7 on the Labour Costs Form give you information about the costs for employees who do not work directly in production. Their wages, salaries and benefits are indirect labour costs.

Column 6. Hours not in production per month

In column 6 on the Labour Costs Form, write down how many hours each employee in the business does work that is not directly in the production of a particular product or service.

At Reliable Tailors:

· Mr Anderson works 80 hours supervising.

· Mrs Hall works full-time in sales and administration.

· Mr Smith works full-time as messenger and cleaner.

· Miss Peters works 40 hours assisting with record-keeping.

Column 7. Pay for time not in production

In column 7 on the Labour Costs Form, write down how much of each person’s monthly pay is for time spent doing work that is not directly related to the production of a particular product or service.

For example, at Reliable Tailors:

· Half of Mr Anderson’s salary, 500 NU, is for supervision which is not directly related to the production of only one particular product.· The full wage for Mr Smith, the messenger, is for work that is not in production.

Direct labour costs per hour

Use the bottom part of the Labour Costs Form to calculate the direct labour costs per hour for your business.

To calculate the direct labour costs per hour:

· divide the total pay for time in production per month (the total of column 5) by the total number of hours worked in production per month (the total of column 4).

At Reliable Tailors, the direct labour costs per hour are 3.30 NU. Look to see how Reliable Tailors do their calculation.

|

|

The direct labour costs per hour tell you how much your employees who work directly in production cost your business each hour. You need this information to calculate the direct labour costs for each product your business makes, or each service your business provides. |

Calculate direct labour costs per item

To do costing you must know the time it takes to make each item and the direct labour costs per hour. Then you can use the Product Costing Form to work out the direct labour costs per item.

Reliable Tailors have calculated that their direct labour costs per hour are 3.30 NU. Now they need to work out how long it takes to make one protective coat. Then they can calculate the direct labour costs for one protective coat.

In Step 2 of the Product Costing Form write down:

· the different activities or types of work your employees do to make the item

· how long each activity takes.

You can see how Reliable Tailors have estimated how long it takes to make one protective coat.

Reliable Tailors estimate that it takes one and a half work-hours to make one protective coat. A work-hour is not always the same as an hour on the clock. It is important to know the difference when you do costing.

The number of work-hours is the total amount of time you need to make one item or provide one service. The time each person works on the item or service is added up to give the total time.

It takes 1.5 hours to complete one coat from cutting to packing. But at Reliable Tailors, each employee only does one activity on each coat. So they can make many coats in 1.5 hours. But it still takes 1.5 work-hours to do all the activities on one coat.

When you know how many work-hours it takes to make one item, you can work out the direct labour costs per item. Do the calculation on the Product Costing Form. To calculate the direct labour costs per item:

· multiply the total work-hours it takes to make one item by the direct labour costs per hour for your business.

Reliable Tailors know that:

· it takes 1.5 total work-hours to make one coat

· the direct labour costs for one hour are 3.30 NU.

So, by multiplying, they calculate that the direct labour costs for one protective coat are 4.95 NU. You can see how Reliable Tailors calculate the direct labour costs for one coat.

STEP 3. CALCULATE INDIRECT COSTS

|

COSTING FOR | |

|

| |

|

STEP 1. |

Calculate direct |

| | |

|

STEP 2. |

Calculate direct |

| | |

|

STEP 3. |

Calculate |

| | |

|

STEP 4. |

Add up |

Reliable Tailors have completed Steps 1 and 2 of their costing. They have filled in part of their Product Costing Form. Now Reliable Tailors know that the direct material costs for one coat are 30.40 NU, and that the direct labour costs for one coat are 4.95 NU.

Indirect costs are all other costs, except direct costs, that you have for running your business, for example, rent and electricity.

Here is how Reliable Tailors calculate their indirect costs:

|

INDIRECT COSTS PER MONTH | ||

| | |

NU |

| |

Rent |

500 |

| |

Electricity and water |

150 |

| |

Maintenance of equipment |

400 |

| |

Insurance (equipment, stock, building) |

200 |

|

A |

Transport |

250 |

| |

Interest on loan |

500 |

| |

Stationery |

20 |

| |

Telephone and postage |

90 |

| |

Advertising and other promotion |

150 |

|

B |

Indirect labour (from Labour Costs Form, total of column 7) |

1830 |

|

C |

Thread, pins, etc. |

100 |

|

D |

Scissors, needles, etc. |

130 |

|

E |

Depreciation |

350 |

| |

Miscellaneous, e.g. teas, cleaning materials |

100 |

| | | |

| | | |

| |

Total indirect costs per month |

4770 NU |

|

|

Different businesses have different indirect costs. Work out how much money your business normally spends for each indirect cost every month. |

Costs that you do not pay every month

You need to calculate indirect costs per month. Your business may have some indirect costs that you do not pay every month, for example, insurance, licences, tools and stationery. For those costs, divide the cost by the number of months the item is used. For example, Reliable Tailors buy stationery such as receipt books every 3 months. They pay about 60 NU each time. So they calculate that their cost per month for stationery is 20 NU:

|

|

Explanations of some of the indirect costs for Reliable Tailors

A. Transport

In the amount for transport, Reliable Tailors include all transport that their business has to pay for. For example, when they:

· collect materials

· deliver finished garments to customers.

Transport is usually an indirect cost because it is difficult to calculate how much the transport costs are for one item. For example, transport costs for one protective coat are difficult to work out because:

· when Reliable Tailors get a delivery of fabric for coats they often get fabrics for other garments in the same delivery· when Mrs Hall uses transport to meet customers, she may sell overalls and other garments, not only protective coats.

B. Indirect labour

Reliable Tailors use information from their Labour Costs Form to get the amount they spend on indirect labour per month. They copy the total amount from column 7 on their Labour Costs Form.

C. Thread, pins, etc.

At Reliable Tailors, thread is an indirect cost because:

· the small amount of thread needed for each garment is difficult to calculate

· the cost of thread for each garment is very small.

D. Scissors, needles, etc.

In this amount, Reliable Tailors include the cost of scissors, measuring tapes and other less expensive equipment or tools which are needed for the business. All costs for less expensive tools and other equipment must be included in the indirect costs.

E. Depreciation

If equipment has a high value and lasts for a long time, you do not write down the cost of buying it. Instead you calculate how much value the equipment will lose every month you use it. This is called depreciation.

Sometimes Reliable Tailors buy expensive equipment like sewing machines. The following section explains depreciation and shows you how Reliable Tailors calculate depreciation in their business.

Depreciation

Depreciation is the loss in value of equipment and is a cost to your business. The total cost of buying the equipment is divided into the number of years you expect to use it.

For some businesses, in particular manufacturers like Reliable Tailors, costs for depreciation are high. So, it is important to include depreciation in the indirect costs for your business.

|

|

Equipment is all the machinery, tools, workshop fittings, office furniture, etc., that your business needs. Learn more about buying equipment in the BUYING chapter. |

Find out if your business has equipment for which you should calculate depreciation

In general, only calculate depreciation for equipment which:

· has a high value, and

· lasts for a long time.

Reliable Tailors calculate depreciation for their sewing machines. They do not calculate depreciation for scissors and other less expensive equipment.

Figure

|

|

What equipment do you have in your business? Do you calculate depreciation for your equipment? |

Estimate for how long you can use the equipment

To estimate how long you expect to use your equipment, you can:

· use your own experience

· ask suppliers

· ask other businesses using the same or similar equipment.

Reliable Tailors have 4 sewing machines. They estimate that they can use 3 sewing machines for 5 years. They bought the fourth sewing machine second-hand and they estimate that they will use it for only 3 years.

Calculate the depreciation

For example, Reliable Tailors paid 6000 NU for sewing machine 1 when they bought it in 1995. They expect to use it for 5 years.

First, they calculate the depreciation per year:

|

|

Then, they divide the amount per year into months:

|

|

Reliable Tailors calculate the depreciation for the other 3 machines in the same way.

If you have more than one machine, or other equipment, add up the depreciation per month for each piece of equipment to get the total amount you need to include in your monthly indirect costs.

Reliable Tailors add up the amounts for depreciation per month for all 4 sewing machines:

Reliable Tailors include the total amount for depreciation per month in their indirect costs.

|

| |

| |

| |

| |

|

|

Sewing |

+ |

Sewing |

+ |

Sewing |

+ |

Sewing |

= |

Total |

|

|

Depreciation is a cost to your business. Learn in the RECORD-KEEPING chapter how to enter depreciation as a cost in your records. |

|

A carpentry business have just bought a circular saw. Help them to calculate the depreciation per month for the circular saw. Here is the information you need: · They paid 4500 Nil for the saw. What is the depreciation per month for the circular saw? |

|

The depreciation per month for the circular saw is 75 NU. |

Calculate indirect costs per item

The total indirect costs for a business must be divided and shared by each product or service the business makes or sells. The indirect costs for one item depend on how long it takes to make that item. The longer it takes to make, the higher the indirect costs for that item.

Normally, the total indirect costs for Reliable Tailors are 4770 NU per month. Reliable Tailors must add a part of the 4770 NU to the costs of each item the business makes.

|

Reliable Tailors’ monthly indirect costs of 4770 NU are shared among their products |

|

|

|

Reliable Tailors make protective coats, overalls and other

garments. |

To calculate the indirect costs for one item use Step 3 of the Product Costing Form. First calculate the indirect costs per hour for all items your business makes.

To work out the indirect costs per hour for your business:

· divide the total indirect costs per month by the total hours in production per month (from the Labour Costs Form).

Then:

· multiply the total time per item (from Step 2 of the Product Costing Form) by the indirect costs per hour.

You can see how Reliable Tailors do their calculations of the indirect costs for one protective coat on the Product Costing Form. The indirect costs for a coat are 7.95 NU.

STEP 4. ADD UP TOTAL COSTS

|

COSTING FOR | |

|

| |

|

STEP 1. |

Calculate direct |

| | |

|

STEP 2. |

Calculate direct |

| | |

|

STEP 3. |

Calculate |

| | |

|

STEP 4. |

Add up |

Reliable Tailors have completed Steps 1, 2 and 3 of costing a protective coat. They now have all the amounts they need to work out the total costs of a coat. To do Step 4, they add up the amounts on the Product Costing Form:

|

Step 1 |

|

Step 2 |

|

Step 3 |

|

Step 4 |

|

Direct |

+ |

Direct |

+ |

Indirect |

= |

TOTAL COSTS |

|

30.40 NU |

|

4.95 NU |

|

7.95 NU |

|

4330 NU |

Now Reliable Tailors know the total costs of a coat. See the completed Product Costing Form.

They follow the same 4 steps for costing all other products they make. They use a separate Product Costing Form for each product. If the costs are not the same, Reliable Tailors use a separate Product Costing Form for each quality or design.

Remember, you only need one Labour Costs Form for the whole business. Reliable Tailors can use the information from their Labour Costs Form for costing all their products.

|

|

The total costs of a product or service are not the price you charge your customers. The total costs are only a starting point to decide what price to charge your customers. Learn how to set your prices in the MARKETING chapter. |

Figure

|

If you are a manufacturer or service operator, go to Costing for a manufacturer or service operator. |

Retailers and wholesalers have the same types of costs and can normally do costing in the same way. Some costs for retailers and wholesalers are different from the costs manufacturers and service operators have:

Figure

|

COSTING | |

| | |

|

STEP 1. |

Calculate direct |

| | |

|

STEP 2. |

Calculate indirect |

| | |

|

STEP 3. |

Add up |

Retailers and wholesalers:

· have direct material costs. Retailers do not make products but they need goods to sell. The costs of buying goods to resell are the direct material costs for a retailer or wholesaler.· do not have direct labour costs. They buy and sell goods made by other businesses. They often have employees assisting in the store but they do not have any employees making products. So, for a retailer or wholesaler, all wages and salaries are indirect costs.

· have indirect costs such as rent and electricity. For a retailer or wholesaler, indirect costs are all the costs the business has except for the costs of buying goods to resell.

Retailers and wholesalers follow 3 steps to calculate the total costs for each product. They can use the Product Costing Form for the calculations.

|

Step 1 | |

Step 2 | |

Step 3 |

|

Direct |

+ |

Indirect |

= |

TOTAL COSTS |

To explain how a retailer or wholesaler does costing we use The General Store as an example.

STEP 1. CALCULATE DIRECT MATERIAL COSTS

|

COSTING | |

| | |

|

STEP 1. |

Calculate direct |

| | |

|

STEP 2. |

Calculate indirect |

| | |

|

STEP 3. |

Add up |

Direct material costs for a retailer or wholesaler are the costs of buying goods to resell.

The General Store calculate the direct material costs per item for the different products their store sells. This is how they calculate the direct material costs for baked beans:

· The General Store pay 36.00 NU for a box of baked beans.

· There are 12 cans in a box.

· The direct material cost of one can of baked beans is 3.00 NU.

|

|

The General Store does not include any cost for transport. They count transport as an indirect cost for the whole business. In the Product Costing Form, The General Store write the name of the product. In column 1, they write how much they pay for one item.

STEP 2. CALCULATE INDIRECT COSTS

|

COSTING | |

| | |

|

STEP 1. |

Calculate direct |

| | |

|

STEP 2. |

Calculate indirect |

| | |

|

STEP 3. |

Add up |

Indirect costs are all other costs that you have for running your business, for example, rent and electricity. For a retailer or wholesaler, indirect costs are all other costs, except costs for buying goods to resell.

The total indirect costs for a business must be divided and shared by each item the business sells. Normally, the total indirect costs for The General Store are 2000 NU per month. The General Store must add a part of the 2000 NU to the costs of each item their business sells.

Figure

The General Store wants to calculate the indirect costs for one can of baked beans. To do this, they must work out the indirect costs charge (%) for their business. Then they can calculate how much to add to the direct material costs for each can of baked beans to cover the total indirect costs.

The indirect costs charge is a percentage that you add to each item you sell to cover the total indirect costs.

|

|

3.00 NU | |

? | |

? |

| |

Direct |

X |

Indirect |

= |

Indirect costs |

|

|

By calculating the indirect costs charge, and adding it to each and every item your business sells, you make sure that you cover your total indirect costs. |

The General Store do the calculations for the indirect costs charge on the top part of their Product Costing Form.

To calculate the indirect costs charge and the indirect costs per item for every product you sell, follow these steps:

1. Calculate total direct material costs per month

2. Calculate total indirect costs per month

3. Calculate the indirect costs charge

4. Calculate the indirect costs per item.

1. Calculate total direct material costs per month

First, calculate how much money your business normally spends each month to buy goods to resell.

The General Store have many regular suppliers. They buy some goods:

· many times a week, for example, bread

· once a week, for example, dry foods and groceries such as sugar, salt and margarine

· once a month, for example, clothes.

They add up the receipts for all the goods their business normally buys during a month.

Some months The General Store buy a lot and some months they only buy a little but normally they buy goods to resell for 10,000 NU per month.

The General Store write the amount for total direct material costs per month at the top of their Product Costing Form.

The General Store does not include any transport costs in the total direct material costs for buying goods. It is difficult to calculate the transport costs for each item. They cannot just divide the cost and add the same amount to each item in the delivery because:

· there can be hundreds of items in one delivery, sometimes more, sometimes less, but the cost for transport is often the same for each delivery· in each delivery, some goods cost a lot and some cost less

· some items are big and some are small.

So, retailers and wholesalers should calculate their transport costs as indirect costs. Below, you can see how The General Store include transport costs as an indirect cost for their business.

|

|

How much money does your business normally spend each month on total direct material costs? |

2. Calculate total indirect costs per month

The General Store work out the total indirect costs for their business per month. Remember, for a retailer or wholesaler, indirect costs are all costs, except direct material costs, that you have for running your business.

The General Store list the indirect costs for the whole business. The list must include all the indirect costs per month for your business.

Here are the indirect costs for The General Store:

|

INDIRECT COSTS PER MONTH | |||

| | |

NU | |

| |

Rent |

300 | |

| |

Electricity |

75 | |

| |

Repairs and maintenance |

50 | |

| |

Insurance |

125 | |

|

A |

Transport |

250 | |

| |

Interest on loan |

150 | |

| |

Advertising and other promotion |

25 | |

|

B |

Indirect labour: |

1 shop assistant |

300 |

| | |

Owner’s salary |

550 |

|

C |

Depreciation |

20 | |

| |

Wrapping paper |

75 | |

| |

Stationery |

10 | |

| |

Licence |

5 | |

| |

Miscellaneous, e.g. teas, cleaning materials |

65 | |

| | | | |

| | | | |

| |

Total indirect costs per month |

2000 NU | |

Different businesses have different indirect costs. Work out how much money your business normally spends for each indirect cost every month. Make sure that your list of indirect costs is complete.

Costs that you do not pay every month

Your business may have some indirect costs that you do not pay each month, for example, insurance, licence and stationery. For those costs, divide the cost by the number of months the item is used. For example, The General Store pay 60 NU per year for a licence to operate the business. The cost per month is 5 NU:

|

|

Explanations of some of the indirect costs for The General Store

A. Transport

The General Store add up all the transport costs that their business has per month. This includes transport costs for:

· visiting suppliers, for example, bus fares and taxis

· buying goods for the business

· delivering goods to customers

· delivery by suppliers.

B. Indirect labour

Retailers and wholesalers buy and sell goods. They do not make any products. They do not have any employees directly involved in the production of goods. So, retailers and wholesalers do not have any direct labour costs. All salaries, wages and benefits for employees and owners are indirect labour costs.

C. Depreciation

Your business should calculate depreciation on equipment that:

· has a high value, and

· lasts for a long time.

For example, The General Store buy a delivery bicycle for their business. The bicycle has a high value of 1200 NU. The General Store estimate that they will use it for 5 years. But the bicycle will lose value during the 5 years. The loss in value is called depreciation and is a cost to the business.

Figure

To work out how much the depreciation of the bicycle costs their business each year, The General Store divide the total cost of buying the bicycle by the number of years they expect to use it:

|

|

Then they divide 240 NU to work out the depreciation per month:

|

|

The General Store write the amount per month in their list of indirect costs.

The General Store write down all indirect costs per month on their list of indirect costs. They add them up to get the total indirect costs per month. They write the amount at the top of their Product Costing Form.

|

|

Make sure that you include all different indirect costs your business has when you do your costing |

3. Calculate the indirect costs charge

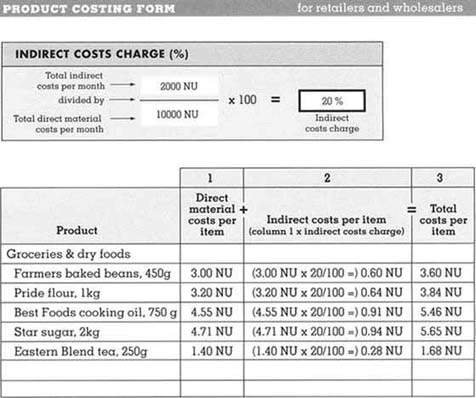

To calculate the indirect costs charge, divide the total indirect costs per month by the total direct material costs per month and multiply by 100. See The General Store’s calculation.

The General Store work out that the indirect costs charge for their business is 20%. The 20% indirect costs charge means that The General Store must add 20% to the direct material costs of each can of baked beans.

|

|

All retailers and wholesalers have different direct material costs and different indirect costs. So, the indirect costs charge will be different for every business. Work out the indirect costs charge for your business. |

4. Calculate indirect costs per item

The indirect costs charge tells you what percentage to add to the direct material costs of all the goods you sell so you can cover your total indirect costs. Now you have to calculate the amount to add to each item.

The indirect costs charge for The General Store is 20%. So The General Store must add 20% to the direct material costs of all the goods they sell.

Here is how they calculate the amount to add to each can of baked beans:

|

|

3.00 NU | |

| |

0.60 NU |

| |

Direct |

X |

Indirect costs |

= |

Indirect costs |

The indirect costs for a can of baked beans are 0.60 NU. Now The General Store know that they must add 0.60 NU to each can of baked beans to cover their total indirect costs.

The General Store use column 2 of the Product Costing Form to work out the amount to be added to each product. They use the same indirect costs charge, 20%, to calculate the amount for all the products their business sells.

STEP 3: ADD UP TOTAL COSTS

|

COSTING | |

| | |

|

STEP 1. |

Calculate direct |

| | |

|

STEP 2. |

Calculate indirect |

| | |

|

STEP 3. |

Add up |

To get the total costs per item, you add up the amounts for direct material costs and indirect costs.

The General Store now has all the information they need to work out the total costs for a can of baked beans.

|

|

Step 1 |

|

Step 2 |

|

Step 3 |

| |

Direct |

+ |

Indirect |

= |

TOTAL COSTS |

| |

3.00 NU |

|

0.60 NU |

|

3.60 NU |

This is how The General Store add up the total costs for baked beans, and for all their other products, on the Product Costing Form:

Figure

|

|

The total costs of a product are the starting point to decide what price to charge your customers. To make a profit, your price must be higher than the total costs of the product. Learn how to set your prices in the MARKETING chapter. |

Every business has costs. Costs are all the money your business spends to make and sell your products or services. Costing is the way you calculate the total costs of making or selling a product, or providing a service.

Costing helps your business to:

· set your prices

· reduce and control your costs

· make better decisions about your business

· plan for the future.

All businesses have two types of costs:

· direct costs

· indirect costs.

Direct costs are all costs that are directly related to the products or services your business makes or sells. There are two types of direct costs:

· direct material costs

· direct labour costs.

Figure

Indirect costs are all other costs, except direct costs, that you have for running your business, for example, rent and electricity. Indirect costs are normally not directly related to one particular product or service. Indirect costs are sometimes called overheads or expenses.

You must understand the different types of costs to be able to calculate the total costs for any product or service your business makes or sells:

|

Direct |

+ |

Direct |

+ |

Indirect |

= |

TOTAL COSTS |

If you are a manufacturer or service operator, use a Product Costing Form and follow 4 steps to calculate the total costs of making and selling any product or service in your business:

Step 1: Calculate direct material costs

Step 2: Calculate direct labour costs

Step 3: Calculate indirect costs

Step 4: Add up total costs.

Use a separate Product Costing Form for costing each product or service.

If you are a retailer or wholesaler, use a Product Costing Form and follow 3 steps to calculate the total costs of each product you sell:

Step 1: Calculate direct material costs

Step 2: Calculate indirect costs

Step 3: Add up total costs.

Retailers and wholesalers do not make products so they do not have any direct labour costs.

Use the total costs of a product as the starting point to decide what price to charge your customers.

Now that you have worked through this chapter, try these practical exercises. The exercises will remind you of what you have learned and help you to improve the costing in your business.

Compare your answers with the Answers. If you find it difficult to work out an answer, read the relevant part of the manual again. The best way to learn is to finish an exercise before you look at the answers. Check the list of Useful Business Words.

|

|

You have learned more about costing in this chapter. But what you have learned does not help you until you use the new knowledge in the day-to-day running of your business. Remember to do the Action Plan to improve the costing in your business. |

|

COSTING AT BEAUTY HAIR SALON This exercise is for manufacturers and service operators. If you are a retailer or wholesaler, do the exercise COSTING AT READER’S BOOKSHOP. Beauty Hair Salon is a service operator. Help Beauty Hair Salon do the costing of a perm. 1. Use the information below to fill in part 1 of the Product Costing Form and to calculate the direct material costs for one perm. To make a perm, Beauty Hair Salon use perm lotion and neutralizer: Perm lotion: · a 5 litre container makes 50 perms Neutralizer: · a 2.5 litre container makes 40 perms 2. Use the information below to complete the Labour Costs Form for Beauty Hair Salon. Then use the information from the Labour Costs Form to fill in part 2 of the Product Costing Form and to calculate the direct labour costs for one perm. There are 4 people working at Beauty Hair Salon: · Miss Mrisho who is the owner of Beauty Hair Salon. She works full-time (160 hours per month) doing hairdressing. Her salary is 1500 Nil per month. The total time needed to make a perm for one customer is one and a half hours. This includes all activities such as shampooing, applying perm lotion, rollers and neutralizer, conditioning, drying and all the rinsing in between.

3. Use the information below to fill in the indirect costs for Beauty Hair Salon. Then do the calculation for indirect costs per item in part 3 of the Product Costing Form for perms. At Beauty Hair Salon: · Rent costs 428 NU per month

|

|

INDIRECT COSTS PER MONTH | |

| | |

|

Rent | |

|

Electricity and water | |

|

Transport | |

|

Advertising and promotion | |

|

Indirect labour (from Labour Costs Form, total oi column 7) | |

|

Depreciation (hair dryer) | |

|

Licence | |

|

Shampoo, conditioner, etc. | |

|

Scissors, combs, brushes, towels, shower caps, perm rods, etc. | |

|

Miscellaneous: cleaning materials, teas, etc. | |

| | |

| | |

|

Total indirect costs per month | |

Figure

|

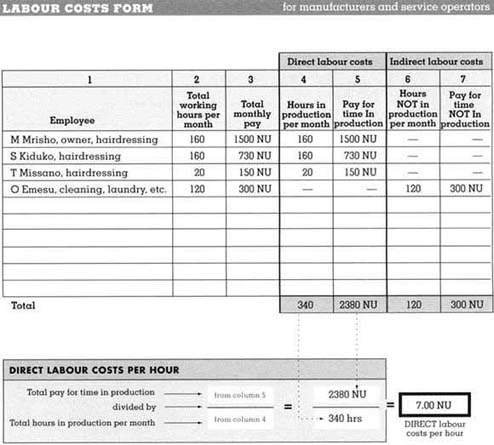

1. Here is the completed Labour Costs Form, list of indirect costs and Product Costing Form for perms:

| |

|

INDIRECT COSTS PER MONTH | |

| |

NU |

|

Rent |

428 |

|

Electricity and water |

200 |

|

Transport |

70 |

|

Advertising and promotion |

75 |

|

Indirect labour (from Labour Costs Form, total of column 7) |

300 |

|

Depreciation (hair dryer) |

20 |

|

Licence |

10 |

|

Shampoo, conditioner, etc. |

100 |

|

Scissors, combs, brushes, towels, shower caps, perm rods, etc. |

50 |

|

Miscellaneous: cleaning materials, teas, etc. |

40 |

| | |

| | |

|

Total indirect costs per month |

1293 NU |

|

· To calculate the costs per month for scissors, combs, brushes, etc. divide the total cost by the number of months they normally use these materials before they buy again, 6 months: · To calculate the costs per month for miscellaneous items, divide the total cost by the number of months they use the items before they buy again, 2 months:

| |

|

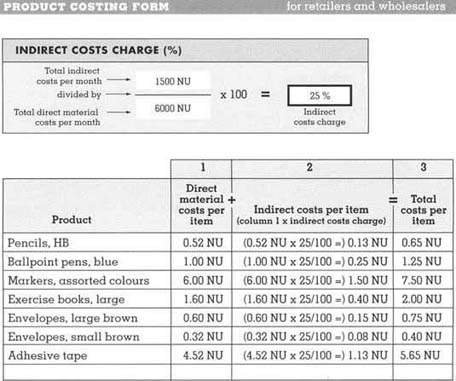

COSTING AT READER’S BOOKSHOP This exercise is for retailers and wholesalers. If you are a manufacturer or service operator, do the exercise COSTING AT BEAUTY HAIR SALON. Reader’s Bookshop is a retail business mainly selling books and stationery. Help Reader’s Bookshop to calculate the indirect costs per item and the total costs per item for each product they have listed on their Product Costing Form below. For your calculations you also need this information: · Reader’s Bookshop normally buy goods to sell for 6000 NU per month.

|

|

The completed Product Costing Form for Reader’s Bookshop should have the amounts shown in the form below:

· To calculate the indirect costs charge, divide the total indirect costs per month by the total direct material costs for buying goods per month and multiply by 100: · To calculate the indirect costs per item (column 2), multiply the direct material costs per item by the indirect costs charge: Pencils: · To work out the total cost per item (column 3), add the direct material costs per item and the indirect costs per item: Pencils: |

|